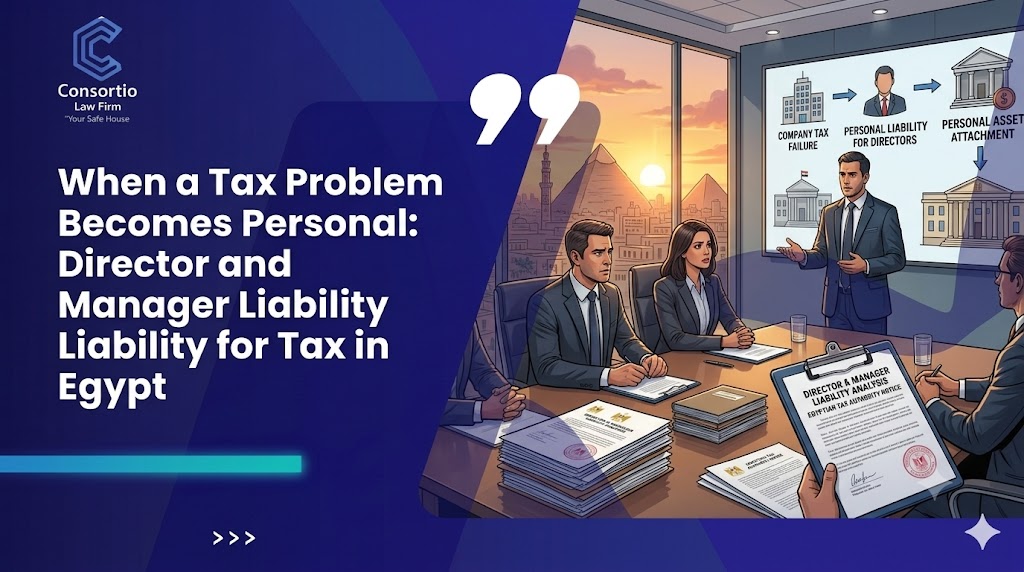

In most companies, tax sits with finance. The directors set strategy, the finance team handles returns and filings, and if something goes wrong with tax, it is treated as a corporate problem — a matter of assessments, fines, and adjustments paid by the company. For businesses operating in Egypt, that mental model is incomplete, and the gap can be career-ending.

Egyptian tax law does not stop at the company. Where a business commits an act of tax evasion, the law reaches through the corporate entity and attaches criminal liability to the individuals who actually run it — and it does so in a way that places the burden on those individuals to clear themselves. For the managers and directors of a multinational’s Egyptian operation, a tax failure can become a personal one, complete with the prospect of imprisonment.

Who the law holds personally responsible

The rule is in Article 73 of the Unified Tax Procedures Law (Law No. 206 of 2020).

Where any act of tax evasion is committed by a legal person, the individual held responsible is the responsible partner, the manager, the delegated managing board member, or the chairman of the board — specifically, those who exercise actual management of the entity. In other words, the law looks past titles to whoever is genuinely in charge of running the business.

And the position is more demanding than it first appears. Under Article 73, the named individual may prove their lack of knowledge of the evasion — which means the starting point is exposure, and it falls to the manager or director to demonstrate they did not know. For someone running an Egyptian subsidiary at arm’s length from group headquarters, “I left tax to the finance team” is not, by itself, a defence; the question is what that person knew or should have known.

Why the threshold is lower than executives assume

The instinctive response is that this only matters for deliberate fraud — and that an honest business with a competent finance function has nothing to fear. That is where many get the risk wrong, because of how broadly Egyptian law defines tax evasion.

Article 68 of the VAT Law (Law No. 67 of 2016) sets out a long list of acts that are deemed tax evasion — and several of them are things a business might think of as merely procedural. They include:

- Failure to register on time with the Tax Authority.

- A registrant’s failure to issue invoices for its taxable sales of goods or services.

- Deducting input tax wrongly, in breach of the deduction rules and limits.

- Obtaining a refund of tax that was not due, knowing it was not due.

- A non-registrant issuing invoices that carry tax.

None of these requires an elaborate scheme. A company that should have registered and did not, or a registered business that fails to issue proper invoices, has — on the face of the statute — committed an act classed as evasion. That is the bridge: an ordinary compliance failure can be characterised as evasion, and once it is, the personal-liability rule in Article 73 is in play.

What personal liability actually means

The consequences of an evasion finding are set by Article 67 of the VAT Law, and they are not administrative.

Tax evasion is punishable by imprisonment of three to five years and a fine — or one of the two — with the offender also jointly liable for the tax and the Additional Tax. The penalty is doubled where the offence is repeated within three years. And critically, evasion is expressly designated a crime involving moral turpitude (a crime against honour and integrity) — a classification that carries professional and reputational consequences in Egypt well beyond the sentence itself, and that can disqualify a person from holding certain positions.

The collateral consequences reach further still. While an evasion case is under investigation, the public prosecutor may direct that government bodies, banks, and public-sector entities suspend their dealings with the taxpayer until the matter is resolved (Article 79 of the Procedures Law). On a final conviction, the Authority may publish the taxpayer’s name in at least two widely circulated newspapers (Article 80). And where the business is a non-resident registrant that fails to meet its obligations, the Minister may ask the prosecutor to block or restrict its access to the Egyptian market altogether until it complies (Article 67 bis of the VAT Law).

There is one procedural gateway worth knowing: under Article 74 of the Procedures Law, no criminal action for these offences may be brought except on the written request of the Minister of Finance or his delegate. That gateway is what creates the window — in practice — to resolve matters before they reach prosecution. But it is a window, not a wall.

The everyday duties that keep you on the right side of the line

Most of this exposure begins with the routine obligations that are easy to neglect — and that, left unaddressed, start the slide from paperwork to evasion.

Registration (Article 25 of the Procedures Law): the business must register within thirty days of commencing activity or becoming subject to VAT. Failure is not only a breach in its own right — it is one of the listed acts of evasion.

Change notification (Article 28): any change to the data submitted on registration — address, activity, legal form, directors, capital — must be notified to the Authority within thirty days (sixty days for heirs in the event of death). Breaching the registration and notification rules draws an administrative fine of EGP 20,000 to 100,000 under Article 71, with a further fine of up to EGP 50,000 for failing to keep the required paper or electronic books for the statutory period.

These fines are levied on the company. But they are also the warning signs: an entity that is careless about registering, notifying changes, keeping its books, and issuing invoices is precisely the entity most likely to find an ordinary failure recharacterised as evasion — at which point the exposure stops being the company’s alone.

What directors and managers operating in Egypt should do

Personal liability is managed through visibility and documentation, not optimism:

- Allocate tax responsibility clearly and in writing, so it is plain who is accountable for what — and so the person in “actual management” is not left carrying undocumented exposure.

- Build real board-level visibility of tax compliance, rather than treating returns and filings as a back-office function the directors never see.

- Keep the routine obligations current — registration, the thirty-day change notifications, invoicing, and book-keeping — because these are both the duties most often missed and the acts the evasion catalogue turns on.

- Document oversight and decision-making, so that, if it is ever needed, the manager or director can actually discharge the burden of showing they did not know of a failure.

- Address any historical exposure early, while the Minister’s-request gateway still leaves room to resolve matters before they escalate.

How Consortio can help

At Consortio Law Firm, we advise the directors and managers of international businesses in Egypt on exactly this exposure — mapping where personal liability could attach, putting in place the responsibility allocation, oversight, and documentation that protect the individuals in management, and keeping the routine compliance obligations current so that an ordinary failure never has the chance to become an evasion question. Where exposure already exists, we work to resolve it while the room to do so remains.

If you hold a management or board position in an Egyptian entity and have never had your personal exposure assessed, that is the gap worth closing. Contact Consortio Law Firm for a confidential review.

Frequently asked questions

Can a director be personally liable for a company’s tax in Egypt? Yes. Under Article 73 of the Unified Tax Procedures Law, where a company commits an act of tax evasion, criminal responsibility attaches to the responsible partner, manager, delegated board member, or chairman who exercises actual management of the business.

Does personal liability only apply to deliberate fraud? No. Egyptian law defines tax evasion broadly. Under Article 68 of the VAT Law, acts such as failing to register on time or a registrant failing to issue invoices are classed as evasion, even though a business may regard them as procedural.

What is the penalty for tax evasion in Egypt? Under Article 67 of the VAT Law, tax evasion is punishable by imprisonment of three to five years and a fine — or one of the two — doubled on repetition within three years, and it is treated as a crime involving moral turpitude.

Can the individual defend themselves? Yes, but the burden is on them. Article 73 allows the responsible individual to prove they had no knowledge of the evasion — which makes documented oversight and clear allocation of responsibility essential.

Prepared by Consortio Law Firm — Your Safe House. This article is provided for general information only and does not constitute legal advice. For advice on your specific position in Egypt, please contact Consortio Law Firm. www.consortiolawfirm.com | info@consortiolawfirm.com | +20 10 2880 6061

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}